Micron

A 25 percent slide has taken the price to a through-cycle multiple. We hold; the entry we want sits near $750.

Micron makes memory chips: dynamic random-access memory (DRAM), the working memory in every computer, and high-bandwidth memory (HBM), the stacked DRAM that sits next to every AI accelerator. An AI-driven shortage has sent memory prices to records, and Micron just printed a blowout: quarterly revenue of $41.46bn, record gross margins, and earnings many times the prior year’s. In the fortnight since the print, profit-taking, an antitrust suit against the three DRAM makers and a rival’s imminent US listing have cut the shares about 25 percent from their high, to $938.38, still up more than 700 percent in a year at a market value above $1tn.

At about ten times this year’s earnings the stock now trades at a normal through-cycle multiple on peak earnings. Memory is cyclical because high prices fund new factories, the capacity lands in a lump roughly two years later, and supply overshoots demand. The market knows this, which is why memory earns its lowest multiples at the very top. It comes down to one number: whether a gross margin in the mid-80s can hold, or whether the wave of new factories now under construction tips the market back into oversupply around 2028. At $938 the price matches our probability-weighted fair value; we hold, and we would add near $750.

The strongest case against us now comes from the dip-buyers. Nothing in the business earned a 25 percent slide: the quarter was a record, the guide went higher, HBM is sold out through 2026, DRAM contract prices rose again in June, and the revenue sits on $22bn of customer commitments under take-or-pay contracts (the customer pays whether or not it takes delivery). The selling came from rebalancing after a huge first half, a lawsuit that will take years, and nerves ahead of a rival’s US listing; several banks have already called the pullback temporary. On this reading, ten times peak earnings for the strongest memory cycle on record is the entry the June price never offered. We grant the mechanics: the selling changed the price, and it left the margin outlook exactly where it was. Our answer is what the price now matches. At $938 the market is paying for our base case, the one where demand stays strong and margins still ease toward the mid-60s. Fair value is a fair deal. The price we want pays us for the bear, and it sits near $750.

- The chokepoint: genuine, controlled by three suppliers, but the product is a commodity whose price swings hard.

- The 12-month direction: roughly balanced; the price sits just below our probability-weighted fair value.

- The entry at today’s price: a shade below fair value, not yet a bargain; the add level sits near $750.

The headline multiple, about 9.7 times this year’s peak earnings, now sits a touch above the through-cycle norm our base case applies. The 12-month fair values against a $938.38 close:

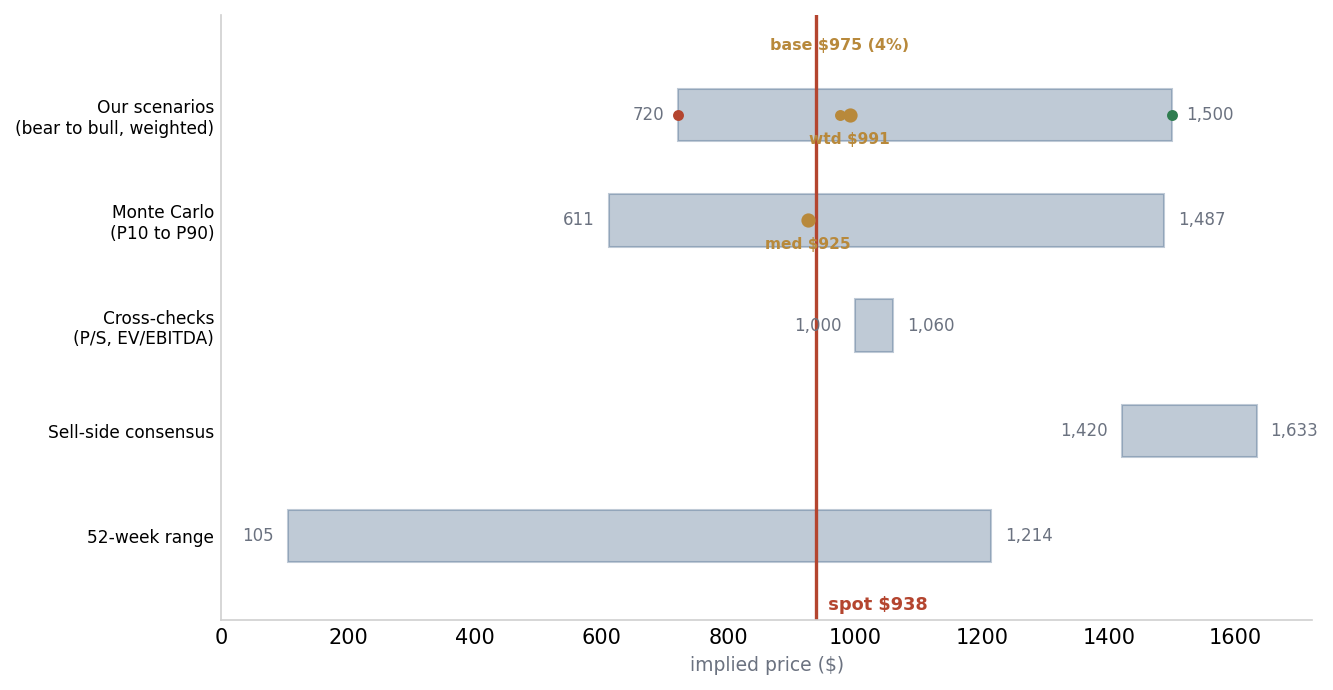

| Scenario | Fair value | vs spot ($938) | Weight |

|---|---|---|---|

| Bear: the 2028 glut | $720 | −23% | 35% |

| Base: margins normalise | $975 | +4% | 45% |

| Bull: the cycle re-rates | $1,500 | +60% | 20% |

| Probability-weighted | $991 | +6% | 100% |

Spot sits just above the $925 simulation median, so the odds of finishing higher are far better than they were at the June high, though still short of even. We would add toward $750, near the bear case, and trim into a move toward the $1,500 bull.

01 Micron holds a real chokepoint on the most cyclical layer of the stack

Micron sits on the memory rung of the AI compute stack, the layer that supplies the DRAM and the high-bandwidth memory stacked beside every accelerator. It is a genuine chokepoint, and the definition matters: an AI training or inference cluster cannot run without memory bandwidth, no substitute exists at the bandwidth AI needs, and the supply is controlled by just three companies. The dependence creates the chokepoint; the three-firm structure decides who collects the rent. Micron, SK Hynix and Samsung together hold about 95 percent of the DRAM market, which is as concentrated as any layer in the chain outside the foundry itself.

A genuine chokepoint inside a tight oligopoly, and the most cyclical link in the stack. After the slide, the price pays for a soft landing in the margin.

The difference between memory and the logic foundry is the cycle. Leading-edge logic is concentrated and its pricing grinds higher; memory is an oligopoly whose product is closer to a commodity, and prices swing violently because capacity is added in multi-billion-dollar fab increments that take about two years to build, so supply arrives in lumps and regularly overshoots demand. Right now that balance is the tightest it has been in a decade, AI has pulled an entire generation of memory into the data centre, and Micron is earning record margins. The chokepoint itself is not in question. What matters is how long the margin it throws off can last.

02 The record quarter has been reported, and the market has traded through it

Unlike the other names in this set, Micron has already delivered its make-or-break print. The fiscal third quarter, reported in late June, was a record on every line, and the fourth-quarter guide went higher still:

| Line | Fiscal Q3 (reported) | Fiscal Q4 (guided) |

|---|---|---|

| Revenue | $41.46bn, over 4× the year-ago quarter | ~$50bn |

| Gross margin | ~85%, against under 40% a year earlier | ~86% |

| Free cash flow (adjusted) | $18.3bn | above $30bn |

The catch is what the market did with it. The quarter was extraordinary, and within two weeks the shares traded below their pre-earnings level anyway. The next print, on 23 September, carries one job: show the margin is holding. The bull case rests on a peak margin proving durable rather than cyclical, so the gross-margin guide is the number to watch, well ahead of the headline.

03 The contract book is the genuinely new feature of this cycle

Three things make this cycle different from the ones before it. The first is structural: a three-maker DRAM oligopoly that has, for now, chosen supply discipline over share wars, which is what lets prices run. Conventional DRAM contract prices roughly doubled inside two quarters at the start of 2026, and industry price trackers expect them to keep climbing through the year.

The second is the HBM seat. High-bandwidth memory is the part of the market AI needs most, and Micron now has a place at the table: it began volume shipments of its newest HBM for Nvidia’s next platform early in 2026. The standing is still modest. SK Hynix holds well over half the HBM market and Samsung is second; Micron’s share, low single digits a year ago, is now around a fifth and climbing fast. The seat is real and improving, but a long way from a lead.

The third is the contract book, the genuinely new thing. Micron has signed sixteen long-term, take-or-pay agreements running three to five years, and added two more since the June print, with General Motors on 1 July and Ford on 7 July, extending the model into automotive memory. The sixteen carry about $22bn of near-term financial commitment and roughly $100bn of revenue through 2030 (the gap is timing, the first a down-payment on the second), backed by around $18bn of customer cash deposits, and they lock in roughly a fifth of Micron’s DRAM and a third of its NAND flash, the storage memory it sells alongside DRAM. That genuinely changes the shape of the downside. It has also never been tested in a real downturn, and that test is the whole question.

04 Record cash is funding the capacity that will end the boom

Micron makes money by selling memory, and at this point in the cycle it is making an enormous amount of it. The third quarter threw off $25.39bn of operating cash flow and about $18.3bn of adjusted free cash flow against $7.1bn of capital spending. Data-centre revenue rose more than seven-fold from a year earlier, and cloud memory revenue more than quadrupled. These are the numbers of a company at the very top of its cycle.

The problem is where the cash is going. The boom that produces the record cash is paying for the capacity that will end it: Micron is lifting capital spending sharply, including a new megafab, and its two Korean rivals are expanding in parallel. That spending is committed at the top of the cycle, which is why a memory balance sheet looks its best just before the turn.

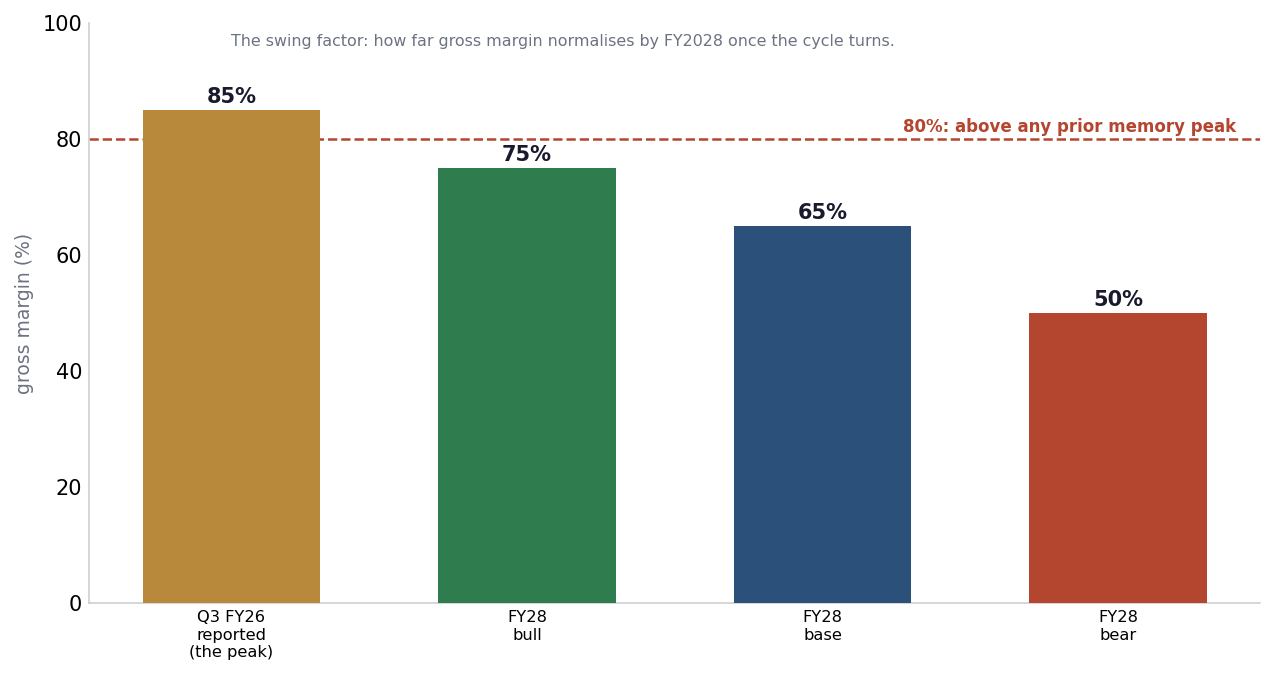

05 The call turns on whether the gross margin holds

Everything comes back to one line: the gross margin. Micron’s reached the mid-80s last quarter and is guided near 86 percent next. The bull case needs that level, or close to it, to hold for years. The bear case is just the industry’s own history: memory has never sustained a margin near today’s for long. Prior peaks topped out far lower, in the 50s and 60s, and even those faded within six to eight quarters as new supply caught up. This run is already that far in. The swing factor is how far the margin falls when the cycle turns, and when that is.

The timing evidence cuts toward caution. Micron’s own chief executive expects industry supply to improve gradually in 2028, which is management itself putting a clock on the tightness. Independent forecasters see DRAM and NAND prices peaking around the middle of 2026 and beginning to roll over as early as 2027, about a year sooner than they had thought. The supply agreements cushion that roll, because a fifth of DRAM and a third of NAND now carry minimum pricing; they cannot prevent it. The question on the September print, and every print after it, is whether the guide defends the mid-80s or begins the walk down toward the 60s our base case assumes.

06 HBM demand runs through a few platforms, and China remains a live risk

The concentration that matters most is in HBM, where the demand runs through a very small number of accelerator platforms. Micron’s HBM fortunes are tied closely to Nvidia’s roadmap, and the competitive set is shifting underneath it: one large accelerator programme has named Samsung rather than SK Hynix as its lead HBM partner, with Micron a smaller participant. A seat that depends on one or two platform winners is a narrower base than the headline memory share suggests.

The contract book concentrates the other way, and more favourably: the take-or-pay agreements spread roughly $100bn of future revenue across sixteen named customers through 2030, backed by cash. That is real diversification of the downside. Geography is the live risk on the other side. Micron’s China business, once around a tenth of revenue and worth roughly $3.4bn, was cut sharply after a server-chip ban, and the memory names remain exposed to export politics on both the demand and the equipment side. The contract book is the strongest concentration story Micron has ever had; the customer and the geopolitics are where it is thin.

07 The market is paying a $1tn-plus valuation for the number-three HBM position

The competitive set is the oligopoly itself, and the positioning differs by product:

| Company | HBM | Conventional DRAM | Role this cycle |

|---|---|---|---|

| SK Hynix | Leader, over half the market | Second | Set the pace of the cycle; lead seat on the dominant accelerator platform |

| Samsung | Second, pushing to regain share | Largest | Swing producer; lead HBM partner on at least one rival accelerator |

| Micron | Around a fifth, from low single digits a year ago | Third | Disciplined number three; gaining share, but not the price-setter |

That ranking matters for the multiple. The market is paying Micron a market value above $1tn, roughly three times what it was worth at the last cycle peak, for the number-three position in HBM and a strong but not leading position in DRAM. The discipline among the three is the single most important variable in the cycle: it is what is holding prices up, and it is exactly the thing that has broken in every prior memory downturn when one player chose share over price. It now faces a test from outside the industry as well: a class action filed in a California federal court in late June alleges the three coordinated to restrict DRAM supply and inflate prices. A complaint is not a finding, and cases of this kind run for years, but it puts a legal price on behaviour the market values as if it were free.

08 The structural risk is a capacity wave landing in 2027 and 2028

The demand backdrop is genuinely strong: AI memory demand is real, HBM is sold out through 2026, and the contract book pulls a large slice of future revenue forward under minimum pricing. The risks sit elsewhere, and there are four of them.

- The capacity wave, with a date on it. Micron is spending above the mid-forty-billion range in fiscal 2027, its Korean rivals are spending in parallel, and the combined industry budget runs well above $54bn for the year, almost all of it new fabrication capacity; Micron broke ground on a western-Japan expansion in the first week of July. It lands in a cluster around 2027 and 2028: management guides supply improving gradually in 2028, and independent forecasters now see prices rolling over as early as 2027. The take-or-pay agreements soften the blow, but a fifth of DRAM under contract leaves the majority exposed to the spot and short-contract market, where a glut shows up first.

- The courtroom. The class action filed on 25 June attacks the supply discipline directly. Damages are one risk; the larger one is behavioural, if a defendant adds capacity or cuts price to blunt the coordination claim.

- Geopolitics. Export rules can shut a market overnight, as China’s server-chip ban already did.

- Valuation. At a $1.06tn market value the stock still has a long way to fall if the cycle turns out to be a cycle; the slide from the June high, 25 percent with no change to guidance, showed how fast the repricing arrives.

None of these resolves in a single quarter, which is why one print can re-weight the call without settling it.

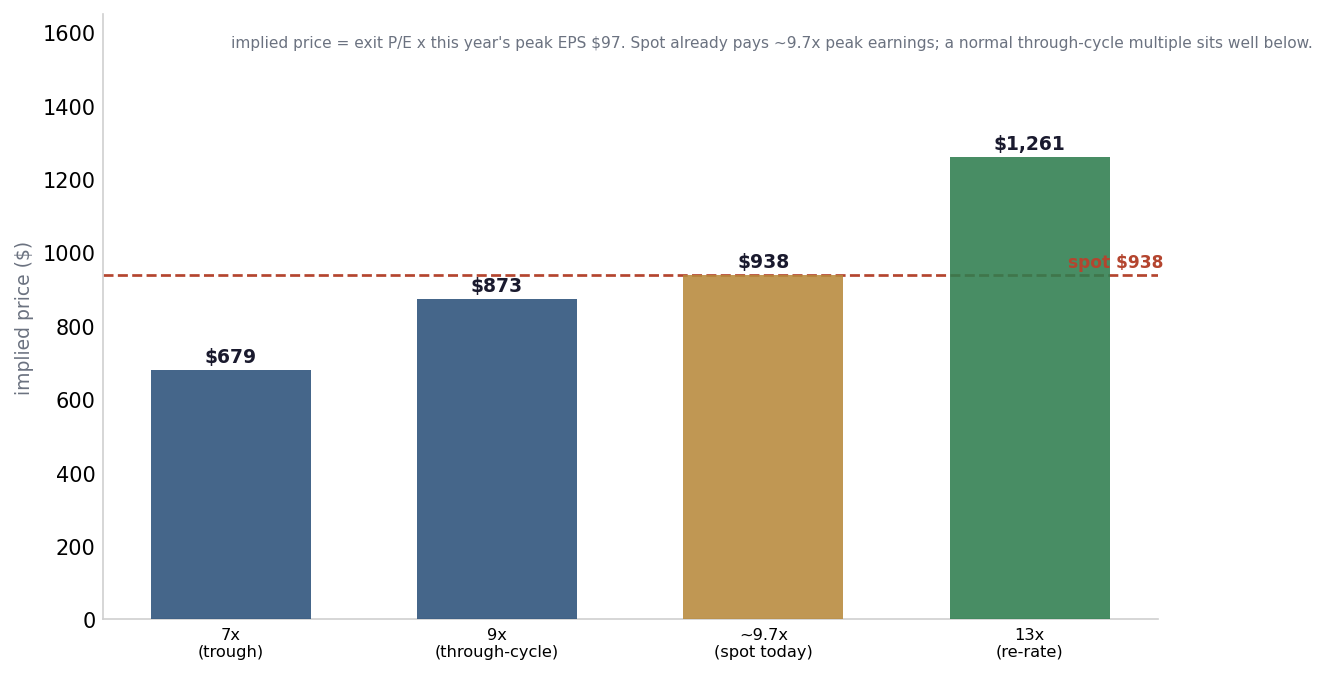

09 A through-cycle valuation now lands just above the price

The reverse lens is the heart of the case. At $938.38 on about 1.13bn shares, Micron carries a market value near $1.06tn. On this year’s peak earnings of roughly $97 a share that is about 9.7 times, down from nearly thirteen at the June high and in line with the multiple memory earns through the cycle. At ten times, the work the multiple used to do falls on the earnings: the price assumes the earnings hold roughly where they are. The test that matters is what a through-cycle valuation produces.

| Exit P/E on this year’s peak EPS (~$97) | Multiple | Implied price |

|---|---|---|

| Trough | 7× | $679 |

| Through-cycle | 9× | $873 |

| Today (spot) | ~9.7× | $938 |

| Cycle re-rates | 13× | $1,261 |

Implied price = exit multiple times this year’s peak earnings of about $97 a share. Spot pays about 9.7 times; the base case adds the mild margin slide the scenarios carry.

Hold earnings near this year’s peak, the contract book and rising volumes roughly offsetting the margin slide, and apply a normal ten times, and the base case is $975, just above today’s price. A sterner nine times, the kind memory earns through the cycle rather than at the peak, is $873, 11 percent below. Cross-checks on sales and on cash earnings land near $1,000 to $1,060, just above spot. The market’s own target sits far higher, anchored on the supply agreements re-rating the whole cycle, the bull scenario rather than the base. Valued through the cycle, the stock trades at roughly fair value; the selloff closed that gap in the first week of July.

10 The scenarios turn on how far the margin falls by 2028

The three scenarios each turn on a single driver: how far the gross margin normalises by fiscal 2028, and what multiple the market pays on the other side.

−23 percent, 35 percent weight. The synchronised capacity wave lands and prices roll from late 2027; gross margin normalises toward 50 percent; earnings near $90 a share at an eight-times trough multiple. The agreements cushion, they do not prevent.

+4 percent, 45 percent weight. AI demand stays strong; gross margin eases toward the mid-60s by fiscal 2028, but volume and the contract floor keep earnings roughly flat, and a normal ten-times multiple, well below today’s, gives $975. The house target.

+60 percent, 20 percent weight. The take-or-pay book holds pricing near the peak, the newest HBM exceeds plan, margins hold in the mid-70s on earnings near $150 a share, and the market pays a higher, utility-like ten times.

Probability-weight the three and the fair value is $991, a few percent above spot, with a simulation median of $925 a few percent below it. The distribution is genuinely two-sided: the bull pays 60 percent, the bear costs 23, which is why this is a hold rather than a short, and the weight of probability now sits at the price rather than below it. The single driver that moves the call is the gross-margin trajectory; the nearer test is the 23 September guide.

11 A 25 percent slide took the price below its pre-earnings level

| Front | This month | Read for Micron |

|---|---|---|

| The blowout | Record Q3, then a guide above $50bn | Extraordinary, and the price fell anyway |

| The tape | A $1,255 high, then 25 percent down | Profit-taking, a lawsuit, a rival’s listing |

| The cycle clock | Forecasters pull the price roll into 2027 | The 2028 debate is starting early |

The two weeks around the print were violent. Micron fell more than thirteen percent on 23 June after a Korean regulator warned on memory-linked exchange-traded funds, rose fifteen percent on the 25 June print to an intraday record of $1,255, then gave it all back and kept going: the shares slid to $975 by 2 July, their lowest since mid-June, and a modest Monday recovery left them at $938.38 on 7 July, about 25 percent below the high and beneath their pre-earnings level.

Three forces drove the second leg. The first was mechanical: profit-taking and half-year rebalancing after a first half in which the main semiconductor ETF rose 72 percent, with hedge funds trimming chip exposure for a month. The second was legal: the class action filed on 25 June. The third was competitive: SK Hynix prices a roughly $29bn Nasdaq listing this week, giving US investors a direct route into the HBM leader, and Michael Burry disclosed a short position in Micron as the slide gathered pace. The consensus target still sits about 50 percent above spot, pricing the bull case as the base. The call turns on the margin, and the next few prints answer it.

- The market traded through the good news. A record print and a raised guide preceded a slide below the pre-earnings level; the burden of proof now sits on margin durability rather than the next beat.

- The crowd is still above us. A consensus average near $1,486 across 45 analysts pays for the supply agreements to re-rate the entire cycle. We treat that as the bull case rather than the base, and the gap closes downward if the margin clock runs out.

12 Verdict: hold at fair value, and wait for $750

- A genuine chokepoint inside a disciplined three-maker oligopoly that controls about 95 percent of DRAM.

- Sixteen take-or-pay contracts, roughly $100bn of future revenue through 2030, backed by about $18bn of customer cash.

- A real and improving HBM seat on the leading AI accelerator platform, with the product sold out through 2026.

- Record cash generation that funds the next generation without dilution.

- A buyback engine arrives in December: CHIPS-agreement cash restrictions expire on 9 December 2026, management has committed to returning excess free cash flow, and one bank models more than $30bn of buybacks in fiscal 2027.

- Even at ten times, the earnings under the multiple are peak-cycle earnings, and the base case needs volume and the contract floor to offset the margin slide.

- A synchronised capacity wave lands in 2027 and 2028; management itself expects supply to ease in 2028.

- Number three in HBM, with a customer base that runs through one or two accelerator platforms.

- A through-cycle valuation lands the base case at spot, leaving only a slim margin of safety at today’s price, and the cycle has always, eventually, turned.

- A class action alleging the three coordinated on DRAM supply attacks the discipline the pricing rests on, a risk to capacity behaviour as much as to damages.

We hold pieces of both, and the gross-margin trajectory decides which confirms. At $938 against a $975 base and a $991 weighted value, the arithmetic carries no lean: the price sits just below fair value, the bull pays 60 percent, the bear costs 23. We stop at hold rather than accumulate because fair value is a fair price, and the entry that compensates for a 2028 glut sits near $750, close to the bear. A hold here means hold what you own rather than buy more. A guide that defends the mid-80s margin would move us toward accumulate; a roll toward the 60s, the first sign of the 2028 glut, or discovery in the antitrust case that reaches supply decisions, would move us toward an outright sell.

13 Scorecard

14 The gross-margin guide decides the next move

▲ Toward accumulate

- A pullback toward $750, close to the cycle-turn bear, where the entry no longer needs the peak to hold.

- A 23 September guide that defends a gross margin in the mid-80s into fiscal 2027, with no sign of a price roll.

- Evidence the contracts hold pricing through a soft patch, the first real test of the new contract model.

▼ Toward reduce

- A gross-margin guide that begins the walk toward the 60s, or contract-price commentary that softens.

- The first hard sign of the 2028 supply wave: a rival’s capacity pull-in, or spot DRAM and NAND prices rolling over.

- Any melt-up toward the $1,500 bull case, which we would treat as a place to trim.

- Movement in the DRAM class action that reaches supply and pricing decisions in discovery, or any sign the suit is changing capacity behaviour.

The one number we track: the gross-margin trajectory through fiscal 2027, and the first sign of the 2028 supply wave. The chokepoint and the contract book are settled questions. Whether the peak margin lasts is the open one, and it is what moves Micron from here. We hold, with the add level parked near $750, and revisit on the September guide.

15 If you want to trade it

A hold offers few natural trades, but the analysis points to some ways to express it. These are ideas to test, not recommendations.

1. Hold within a band: trim toward $1,500, add toward $750. Even after the slide the stock is up more than 700 percent in a year, and the price now matches a base case in which margins ease while volume and the contract floor hold earnings roughly flat. The real test plays out over several prints, and a hold means waiting for the band: trim into strength toward the $1,500 bull case, and add only on weakness toward the $750 re-entry level, near the bear.

Risk: the contracts hold pricing and the cycle re-rates before any pullback, leaving a patient buyer behind.

2. Pair trade: long SK Hynix, short Micron (relative value). The clean memory pair arrives this week. SK Hynix lists American depositary receipts on the Nasdaq around 10 July in a roughly $29bn offering, which removes the access friction that has kept the pair off most US books. Hynix holds about 60 percent of the HBM market against Micron’s fifth and the lead seat on the dominant accelerator platform, so a small, beta-aware long-Hynix, short-Micron pair expresses the HBM ranking directly, without a view on memory’s direction. The old alternative, fading Micron against TSMC and Nvidia, has weakened: the slide has already pulled much of that premium in.

Risk: Micron is the share gainer in HBM, so the gap the pair rests on narrows over time; listing-week flows are noisy in both directions; and both legs are defendants in the same antitrust suit, so the case moves them together.

3. Buy a put spread into the 23 September print (high conviction only). The case here has weakened: at $938 a bearish structure bets on the bear scenario itself rather than on a reversion the market has already delivered. Around the print Micron’s realised volatility ran near 120 percent annualised, and it routinely moves ten percent or more on a result, so an outright short is dangerous and the borrow is unforgiving. An investor who shares the downside tilt can buy a put spread into the 23 September print, capping the cost in advance. One caveat on the data: the reported implied volatility looks stale and the historical earnings-move sample is too small to trust, so price the structure off how violently the stock actually moves, not off a screen.

Risk: a blowout guide that defends the margin can gap the stock straight up through the structure; defined risk caps the loss, but the bull tail toward $1,500 is real.

Above all, size it small. Micron carries a beta near one and a half to the chip index and moves violently around prints, and the debate it turns on, whether a peak margin can hold into 2028, resolves over several prints rather than one. The first idea fits a hold best; the pair is tactical; the options route is for high conviction only.

16 Dates to watch

The events that move Micron or its read-through over the coming weeks:

- 10 Jul 2026: SK Hynix lists on the Nasdaq. A roughly $29bn ADR offering puts the HBM leader on a US exchange for the first time; the debut tests whether money rotates out of Micron or the listing lifts the whole memory complex.

- 29 Jul 2026: SK Hynix results. The HBM leader and the clearest read on memory pricing, HBM demand, and whether the three makers are still holding supply discipline.

- 26 Aug 2026: Nvidia results. The customer whose accelerator roadmap sets the HBM order book; the demand read that underwrites the whole memory cycle.

- 23 Sep 2026: Micron fiscal Q4 results. The main event. The beat itself is expected; the read is the gross-margin guide and the first fiscal-2027 signal, the test of whether the peak margin holds.

- through 2026 and 2027: spot DRAM and NAND contract prices, and the first hard signs of the 2027 to 2028 capacity wave, the deciding variable for the call.

Dates from company IR calendars and reported schedules as of 7 Jul 2026; confirm against each company’s IR page, as dates can shift.

Not investment advice. For information and discussion only, and not a personal recommendation, offer or solicitation. Capital is at risk, and investments can fall as well as rise. The scenario fair values and price targets here are the publisher’s estimates, not a forecast or a guarantee. Do your own work.

All figures come from Micron’s public disclosures, public market and industry data, and the publisher’s own calculations. No third-party broker or expert-network research is quoted or reproduced. Sources: Situational Awareness; Micron public disclosures; chokepoints.ai scenario and valuation work. © 2026 chokepoints.ai · Issue 005 · Micron is the US memory maker at the top of an AI super-cycle; a July slide took the price to a through-cycle multiple, and the call now rests on whether peak margins hold into 2028. All issues