Powertech

A real AI-packaging chokepoint, priced for a flawless ramp.

Powertech (PTI) does the last step in making a chip: it takes the finished silicon and packages and tests it so a computer can use it. It is Taiwan’s second-largest at that and the world’s fifth, and the leading specialist in packaging memory chips.

The AI twist is newer. The tightest bottleneck in an AI accelerator is no longer the transistors; it is the advanced packaging that wires the chip out to the rest of the system. TSMC’s version of that step, chip-on-wafer-on-substrate or CoWoS, is sold out and mostly goes to NVIDIA. Powertech is building a credible alternative on large panels, and AMD and Broadcom are reported (in trade press, not confirmed by either company) to be evaluating it, so it could work as an overflow valve for the AI demand TSMC cannot meet. Trade reporting puts that capacity booked through 2027, behind a record 2026 capital budget of about NT$50bn (US$1.6bn).

The market has paid for most of it. The stock has nearly tripled off its 52-week low, and after peaking near NT$387 it trades at NT$333.5, about 14% below that high and roughly 4.2 times its net asset value on an 11% return on equity. The question is no longer whether the chokepoint is real. It is whether enough has now come out of the price. Our answer: not yet.

We run this newsletter on a structurally bullish view of the AI build-out. So we set ourselves a hard test on Powertech: put our own worldview into the valuation, and see whether it still says buy. It does not, even on our own bullish inputs. The price already pays for the ramp, and that is the most useful thing we can tell you about it.

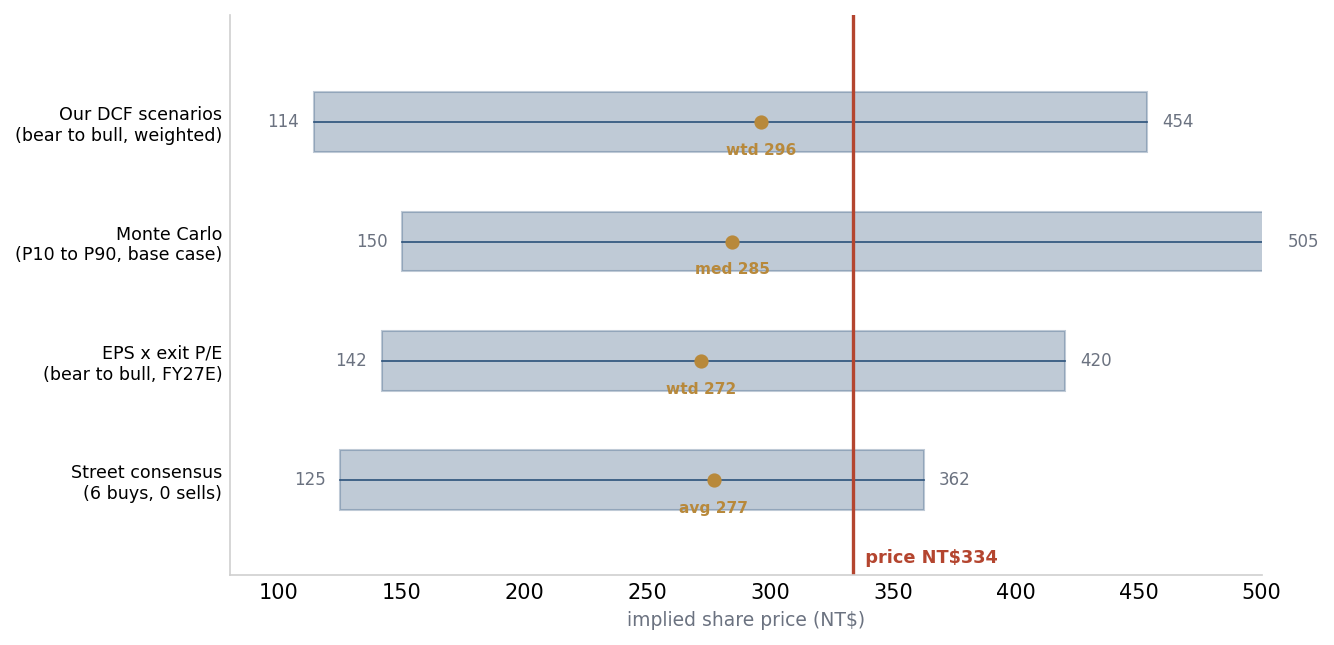

A quality AI advanced-packaging beneficiary that has given back part of its run, but the price still leads the value. Every lens we run sits below spot: a structural-demand DCF on our own bullish inputs puts fair value near NT$296, the Monte Carlo median is NT$285, the EPS cross-check NT$272 and the Street average NT$277. So we are not buyers at NT$333.5. We accumulate toward NT$272 to NT$285, about 15 to 18% lower, or on hard proof the FOPLP ramp is converting to margin. The bull case (NT$420+) needs a flawless ramp the price does not pay you to underwrite.

01 Stack: the #2 memory OSAT, and a CoWoS overflow valve

A short primer. OSAT stands for outsourced semiconductor assembly and test. Chip designers design the silicon; foundries print the transistors; OSATs do everything after the wafer leaves the cleanroom. They cut the wafer into individual die, mount each die on a substrate or interposer, wire it up, encapsulate it, and run the burn-in and final test. The packaging step is increasingly where the value lives, because as transistors get smaller the bottleneck migrates upstream into how you wire a chip to the outside world.

PTI is Taiwan’s #2 OSAT and the world’s #5, with about 5.5% of the global OSAT market in 2024. It is the leading specialist in memory-IC packaging and test for DRAM and NAND, and its customer base is anchored by all three global DRAM leaders, Samsung, SK Hynix and Micron, who outsource portions of their memory packaging to it.

Two things to note about that customer mix. First, the DRAM leaders do not outsource everything; the highest-value memory packaging, particularly HBM stacking, stays largely in-house. PTI does not own the HBM TSV stack. Second, Micron acquired PTI’s Xi’an back-end facility in 2023 to internalise its China memory packaging. That cuts against a simple single-customer Micron-dependency story.

So what is the chokepoint? Two of them. The first is conventional memory packaging, cyclical and competitive, riding the DRAM and NAND volumes of the AI server build-out. The second is the interesting one: advanced packaging for AI logic chips. When an AI accelerator needs to be packaged, die-on-interposer, with thousands of connections per mm², the dominant solution is TSMC’s CoWoS. CoWoS is sold out. It is the binding constraint on AI accelerator supply today. NVIDIA is the dominant customer; AMD, Broadcom and the custom-ASIC programmes form the queue behind it, and that non-NVIDIA queue is the natural overflow pool. Anyone building a credible alternative is, in effect, building an overflow valve. That is what PTI has done.

02 Technology: PiFO is a credible second source with no monopoly attached

The technology is the moat, so here is the technical bit. Fan-out wafer-level packaging embeds the die in a moulded wafer with redistribution layers, fine copper wiring that fans out from the die’s tiny contacts to larger package pads. Shorter interconnects, better electrical performance, lower cost at scale. Panel-level packaging (FOPLP) does the same on large square panels rather than circular 300mm wafers. The area-efficiency gain is enormous, but panel processing is hard; yields collapse if the panel warps, and only a handful of players are credible at it.

PiFO is PTI’s FOPLP architecture, with redistribution layers on both sides of the die. Trade reporting frames it as rivalling TSMC’s CoWoS-L; be precise about that. PiFO is a mould-compound panel fan-out, not a silicon interposer, so it is better read as a CoWoS-S/R-class alternative for AI-logic packages that do not need a large interposer, while the very largest accelerators stay on CoWoS-L. The distinction sets the runway: as flagship accelerators get bigger, more of the package volume migrates to CoWoS-L, the lane PiFO does not serve. Trade reporting put trial yields at 90% in September 2025 and at 95% by June 2026, with customer validation due in 2H 2026. Two caveats belong next to that figure: no broker source we have seen corroborates it independently, and a qualification yield on early product is not a volume yield; peer-reviewed work on large panels puts die-shift near 19 microns at the panel edge, which is exactly the failure mode that decides whether fine-pitch panel packaging survives mass production. The number that matters is sustained production yield at volume, and nobody outside the company has printed it.

On the demand side, the public reporting is that several major US AI chipmakers have turned to Powertech for the overflow, and that AMD and Broadcom back its FOPLP, with monthly FOPLP revenue targeted toward about NT$3bn. At announcement, in late 2025, that capacity was reported fully booked with demand near twice planned supply. The freshest broker channel checks, from spring 2026, are softer: clients adjusting quarterly orders, and FOPLP revenue estimates for 2026 and 2027 being trimmed. Booked is not the same as shipped, and the order book has already breathed once.

Three honest caveats. The AMD and Broadcom interest is reported, and brokers still class the datacenter engagements as market speculation rather than wins; the one confirmed AMD project is a console gaming APU, and Broadcom’s TPU packaging sits with TSMC and MediaTek. The order book is only partly visible; the full customer mix is undisclosed, so take it seriously but do not size it precisely. FOPLP is contested, not a monopoly: ASE is also expanding FOPLP capacity and TSMC has been preparing a CoPoS pilot line for 2026. PTI is one credible second source among several, which caps the long-run margin pool even as it leaves the next 18 months intact. And the HBM nuance matters: the HBM TSV and 3D-stacking process stays largely captive at the memory makers. The memory TSV and 3D-stacking packaging market is expected to grow from roughly US$2 to 3bn in 2024 toward US$10 to 15bn by 2028, but that growth accrues primarily inside the memory makers, not at PTI.

03 Numbers: the memory upcycle is already in the prints

The conventional half of the business is firing. Q4 2025 revenue was NT$21.41bn, up about 25.2% year on year, with net income of NT$1.86bn, up about 22.3%, its strongest quarter in three years. Q1 2026 sales were NT$21,314m, up about 37% year on year, with net income of NT$1,844m versus NT$1,175m a year earlier, up about 57%. April 2026 revenue reached NT$7.58bn, up about 32.5% year on year, and May followed at NT$7.92bn, up 30.2%, the fifth straight month in which the growth rate has come down. June lands by 10 July.

Be honest about the shape. Q1’26 net income (NT$1,844m) was essentially flat on Q4’25 (NT$1.86bn). The big year-on-year numbers are real, but they lap a weak 2025 base; this is a strong upcycle level; a sequential inflection has yet to show. The inflection the bulls need is the FOPLP ramp in the second half.

The context is a memory market in full upcycle. The HBM market is projected to grow from roughly US$35bn in 2025 toward US$45 to 55bn in 2026, with estimates varying by research house. PTI is a leveraged way to play that cycle without backing a single memory maker, because it packages and tests for all three. A reported dividend yield of about 2.6% is a modest cash return while the capex bet is in flight, and FOPLP spending could pressure even that if free cash flow stays negative through the ramp. The risk on this leg is duration, not direction: the prints are clean now, the question is how long the cycle holds in 2026.

04 Capex: a foundry-grade bet funded on OSAT earnings

This is where the hold gets uncomfortable. Management is putting real money behind PiFO: PTI raised its 2026 capex guidance to about NT$50bn (~US$1.6bn) in April 2026, up from an earlier NT$40bn plan and roughly double the prior year, primarily to expand FOPLP. Here is the number that should give a value-conscious investor pause. NT$50bn of capex against a revenue run-rate around NT$85 to 90bn is roughly 45 to 55% of revenue. That is at or above the top of foundry-grade capital intensity: across the recent build-out TSMC has run about 33 to 48% of revenue, peaking near 48% in 2022, and OSAT peers run 10 to 18%. PTI is spending like a leading-edge foundry on the earnings base of an OSAT.

The new panel lines in Hsinchu, P11 plus P12 (a former AUO display fab acquired for NT$6.9bn), carry the build-out, with a target of about 6,000 panels per month. The timing needs stating precisely, because the market has at times traded this as a mid-2026 story: first-phase panel equipment arrives over the summer of 2026, the chairman puts customer qualification in the second half, and volume shipments start from 1H 2027, building through that year. FOPLP is a 2027 revenue story with a 2026 proof-of-life. A capex programme of this size at a company earning roughly NT$8 to 9bn a year in net income is a heavy lift: NT$50bn is close to six years of current net income in a single year. Free cash flow will be negative through the heavy ramp in 2026, and the gap has to be funded, by the balance sheet, by debt, or eventually by equity, none of which the bull case prices. The whole ROE bridge depends on that NT$50bn converting into revenue at FOPLP margins. If it converts, the spend buys a seat in the AI advanced-packaging pool. If it does not, it widens an asset base that still earns an OSAT return, and the multiple compresses.

05 Valuation: every lens lands below today’s price

PTI traded at NT$333.5 on 2 July 2026, a market capitalisation of about NT$246bn on 738.8m shares, nearly triple its 52-week low of NT$116 and about 14% below an all-time high near NT$387. The run has been a brutal re-rating: from pricing PTI as a memory OSAT to pricing it as an AI advanced-packaging capacity owner, and the late-June round trip, NT$387 to NT$311 and back above NT$330 inside three weeks, is the market testing how much of that re-rating is durable. Book value per share is about NT$79, putting the stock at roughly 4.2× book on an ~11% ROE. That multiple only makes sense if the capex bet lifts ROE materially and the FOPLP mix expands margins structurally. That is the right debate. It is also a debate that has already been had, in price.

Our cross-check runs FY27E EPS against a justified exit multiple, discounted one year at 10%. These EPS figures are judgemental, a scenario frame rather than a bottom-up segment model, and the biggest swing factor is the exit multiple:

−57%. The capex bet disappoints, FOPLP yields stall, ASE or TSMC CoPoS take share, the memory cycle turns, and the multiple compresses to a 13× OSAT trough.

−21%. The ramp works, margins expand as panel volumes scale, and the multiple settles to a 17× OSAT mid-cycle. Still a loss from here.

+26%. PiFO scales as a structural second source on a higher EPS base, at a 21× multiple.

Prob-weighted at 25/50/25, the EPS-model target is about NT$272, roughly 18% below spot; the July rebound has re-opened the gap the late-June pullback had briefly closed. If you believe PiFO earns a durable second-source re-rating and holds 28 to 30× on bull EPS, the upside tail is roughly NT$560 to 600; we exclude that from the headline because we do not think a panel fan-out second source holds a foundry multiple, but an honest reader should know the tail exists.

The Street has not caught up, and that cuts against the bull, not for it. Consensus targets range from about NT$125 to NT$362.5, average near NT$277, on 6 buy ratings and 0 sells. At NT$333.5 the price sits above the average but below the NT$362.5 high, and with zero sells there is no downgrade cushion: on any print miss, the next move in consensus is down, not up. You are not buying what the Street has not priced; you are buying what the Street is already long.

5b Worldview: even our bullish DCF lands below spot

Here is the honest objection to everything above. We run on a structurally bullish view of the AI build-out, a front-loaded, decade-long trajectory rather than a cycle. So is the hold just an artefact of conservative, mean-reverting assumptions? If we let our own worldview drive the numbers, does PTI become a buy?

We tested exactly that. Instead of an exit multiple, we built a multi-stage free-cash-flow model and put the worldview into the demand path: structural revenue growth, margins expanding as the FOPLP mix rises, and, crucially, capex modelled explicitly, gliding from roughly 55% of revenue in 2026 down toward 15% as the build-out matures. That is the right way to value a capex-heavy name. The bet is spend now, harvest the structural demand later, and a DCF is the only honest way to see whether it pays at NT$333.5.

−63%. The consensus prior: AI demand treated as a cycle that rolls over mid-decade.

−6%. Structural growth, margins to ~16% as FOPLP mix rises.

+46%. The build-out accelerates, PTI holds its panel niche, margins reach ~18%.

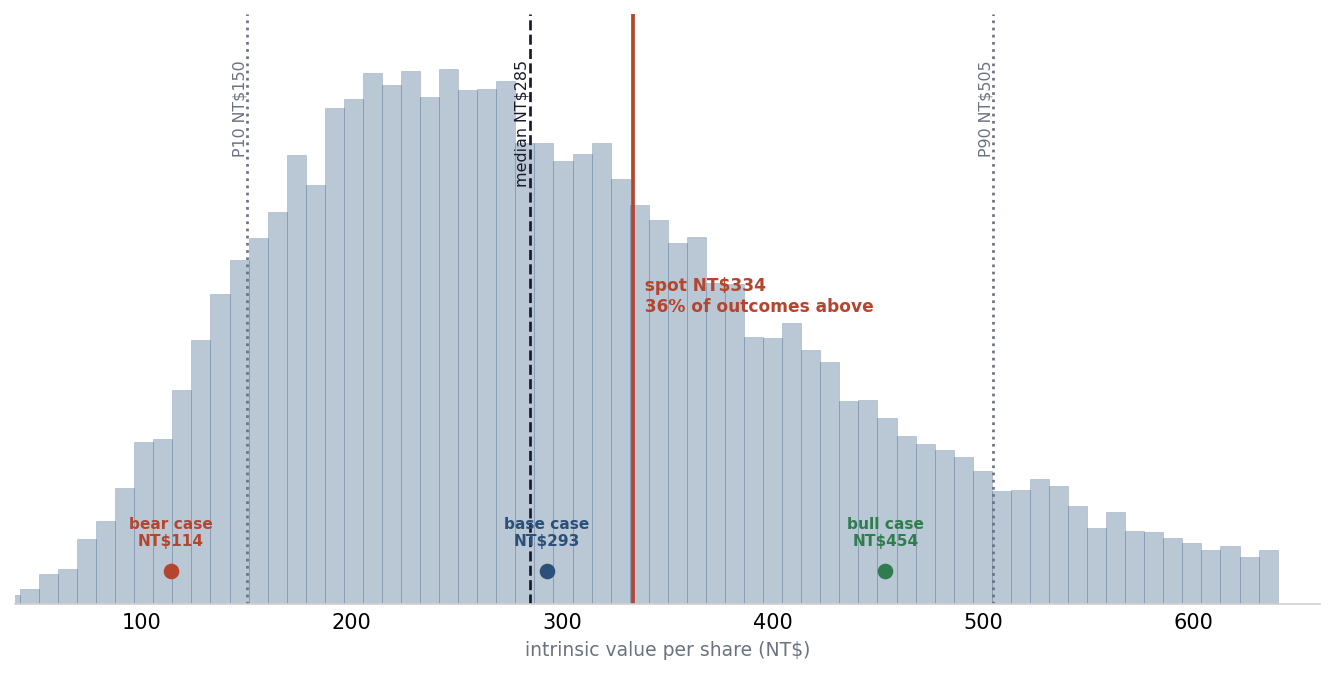

Weighting these 30/45/25, deliberately tilted toward our structural view, gives an intrinsic value of about NT$296, roughly 11% below spot. A Monte Carlo over the drivers (growth, margin, capex normalisation, discount rate) puts the median at about NT$285 and gives a 36% probability that intrinsic value clears today’s price.

Then the clincher. Run it in reverse. At NT$333.5 the market is pricing roughly a 16.0% five-year revenue CAGR, back above our structural base-case path of about 15.4%. In mid-June, at NT$363.50, the market priced more growth than even our bullish base case; the late-June pullback briefly took implied growth under our base, and the July rebound has pushed it back over. Even on our own worldview the stock is more than fully priced, with about 36% of our Monte Carlo outcomes clearing the price and the clear majority below it. That is not the margin of safety we need to fund a name burning cash for two years on foundry-grade capex while it shares the durable rent with a bigger overflow winner. We are not buyers at NT$333.5; the level that pays us for that risk is nearer NT$285, some 15% below here.

06 Market tape: louder demand, a cheaper stock, a more crowded packaging race

A note is anchored to a moment, so we read the live tape for the memory cycle, the advanced-packaging race and PTI itself, and map each event to the call.

The demand leg, the part we called the free option, got distinctly louder. TrendForce has conventional DRAM contract prices rising 58% to 63% in Q2 2026 after a 93% to 98% jump in Q1, with NAND up as much as 75%, and Micron’s 24 June quarter printed record revenue of about $41.5bn, more than four times the year-earlier figure, at a record gross margin near 85%, a once-in-cycle print, with supply called tight into 2028. PTI is the number-two memory packaging and test house, and that volume is already in its prints: April 2026 revenue rose 32.5% year-on-year and Q1 sales about 37%. The conventional memory-OSAT business that does the work while FOPLP is the upside is geared straight to this, and a cycle called tight into 2028 lengthens its runway.

The competitive leg, which is where our bear case lives, got more crowded in the same window. TSMC is expanding CoWoS and SoIC hard and has a CoPoS panel-level pilot line completing around June 2026, with mass production targeted for 2028 to 2029; ASE is accelerating a 310mm fan-out panel line, PTI’s most direct competitor. Read together they set the clock precisely: PTI has roughly a two-year FOPLP window before TSMC’s panel-level packaging and a larger rival compete head-on, which is exactly the booked-through-2027, unproven-beyond-it risk in the bear column. The reported AMD and Broadcom interest is the bull’s answer, a reason PTI might hold a seat outside TSMC’s walled garden, but it rests on trade-press reports of evaluations, with no confirmed win, and it does not extend the window.

The setup is the important part. PTI first de-rated through this news, from NT$363.50 to NT$311, then snapped back above NT$330 as the memory prints landed. The round trip matters: at NT$333.5 the market again prices about 16.0% five-year growth against our 15.4% base, so the brief window in which the tape was cheaper than our worldview has already closed. Every lens sits below the price once more, and the move is away from our accumulate line, not toward it. Three cautions keep this a read-through only.

- The HBM stack is not PTI’s to package. The biggest memory dollars sit in HBM, and the HBM stack stays captive at the memory makers. PTI benefits through conventional memory packaging and test and the broader logic-packaging pull; the HBM stack itself passes it by, so the loudest part of the cycle flows to it the least.

- The second-source race tightened inside a fortnight. Trade reporting on 25 June has ASE’s automated FOPLP line targeting mass production by the end of 2026, against PTI’s qualification-then-1H27 schedule, roughly two quarters ahead; on 18 June TSMC and Amkor signed a definitive ten-year Arizona packaging agreement; and on 1 July ASE raised CoWoS and FoCoS quotes by more than 20%. Overflow pricing power is real and being printed, but the bigger rivals are monetising it first, and broker research now scores ASE and Amkor as the winners of the high-end overflow race while PTI’s lane runs through ASICs, CPUs and memory-adjacent work. One offset runs the other way: mid-June checks have TSMC’s CoPoS slipping, with volume production now unlikely before 2029 to 2030, which lengthens the panel window for everyone already standing in it.

- A cyclical tailwind is not the structural re-rating. The free option getting louder does not prove the FOPLP capex bet works; that is still PTI’s own execution, the qualification-and-ramp schedule we track at the end. A peak keeps the prints strong for a few quarters. It is no reason to pay past our margin of safety below about NT$285.

So the tape improves the demand half of the call and sharpens, rather than settles, the durability half. It pushes PTI toward our accumulate line, not past it. The print that moves our number next is PTI’s own, due in late July (June monthly sales land by 10 July), where what matters is whether the FOPLP mix lifts margins toward the high teens. Another revenue beat on its own tells us little.

07 Both sides: the price is paying for the bull

- The binding constraint is real and the overflow valve is being paid for. CoWoS is sold out; FOPLP is the credible second source scaling in the right window, with AMD and Broadcom reported to be evaluating it. Capacity was reported fully booked at announcement, and ASE lifting advanced-packaging quotes by more than 20% on 1 July shows the overflow pricing power is real and being printed.

- The capex is the moat. About NT$50bn in 2026 is a barrier to entry; ASE is a larger incumbent with a different mix, and TSMC’s CoPoS is a 2026 pilot, not a ramp.

- The memory upcycle is a free option. The HBM market goes from roughly US$35bn in 2025 toward US$45 to 55bn in 2026; the conventional memory-OSAT business does the work while FOPLP is the upside.

- The numbers are moving. Q4 2025 was the strongest quarter in three years; Q1 2026 sales up about 37% YoY, net income up about 57%; April revenue up 32.5% YoY.

- The Street is still behind. Six buys, zero sells, average target ~NT$277, with earnings revisions still to come as prints beat.

- The CoPoS slip is PTI’s friend. Mid-June checks push TSMC’s panel volume out toward 2029 to 2030, which lengthens the window for the panel lines already standing.

- The easy money has been made. The stock has nearly tripled off its 52-week low; the deep mispricing was in the other direction a year ago, and the pullback from the high is the first sign the re-rating has run ahead of itself.

- You are paying for an ROE step-change not yet delivered. A ~23× forward multiple and ~4.2× book on an ~11% ROE is a re-rating the capex still has to earn. If the panels do not fill, the multiple compresses first and book support is well below.

- In 2026 the capex is an FCF problem first; the moat comes later, if it comes. Roughly 45 to 55% of revenue means negative free cash flow through the ramp; the equity has to hold through a year of ugly prints.

- FOPLP is competitive, not captive, and PTI may be the second second-source: ASE’s automated line targets mass production by end-2026, about two quarters ahead of PTI’s 1H 2027, and Amkor just signed a ten-year TSMC Arizona agreement. Pricing power is real in 2026 to 2027; it is not obviously durable into 2028.

- Order durability is already being tested. The late-2025 “fully booked” book has breathed: spring channel checks in broker research show clients adjusting quarterly orders and FOPLP estimates being trimmed, and beyond 2027 the same customers may route to CoPoS, qualify ASE, or in-house.

- HBM is the biggest miss in the bull narrative. The HBM TSV stack stays captive at the memory makers; PTI does not own it. A memory turn hits conventional packaging and compresses the premium on the FOPLP mix.

- PiFO serves the smaller lane, and it is shrinking. Panel fan-out fits CoWoS-S/R-class and disaggregated chiplet parts; the large-interposer CoWoS-L flagships stay out of reach. As accelerators get bigger, more of the value migrates to the lane PiFO cannot serve.

- The Street has already done its upgrading. The high target is NT$362.5 and the average is around NT$277; at NT$333.5 the price now sits between them rather than at the top, so the easy upgrade-driven leg is behind it.

Both halves are real. The whole call is which half the price is paying for, and at NT$311, after the pullback, it is much closer to paying for the base case than the bull.

08 Scorecard

Best-in-class AI advanced-packaging beneficiary, and the chokepoint survives scrutiny. But even on our bullish worldview the price still leads the value on every lens. We are not buyers at NT$311; we accumulate the structural thesis toward NT$272 to NT$285, or on hard margin proof from the P11 ramp.

09 Triggers: what would move us to buy or sell

▲ To buy (a lower price, or the bull proven)

- A pullback below ~NT$285 (toward NT$260 to 285) on a memory-cycle wobble or a FOPLP yield hiccup that does not break the order book. That is around our worldview-weighted fair value, with a real margin of safety on the structural thesis.

- Evidence pushing into the bull case (intrinsic ~NT$454): Q2’26 or Q3’26 prints showing the FOPLP mix expanding margins toward the high-teens, beyond another plain revenue beat.

- Customer qualification landing in 2H 2026 and volume shipments starting on the 1H 2027 schedule, with named, durable customers and contract duration disclosed past 2027.

▼ To sell

- A FOPLP yield reversion below the ~90% trial mark, or a delay in P11/P12 commissioning.

- TSMC CoPoS scaling faster than expected, or an ASE FOPLP win that compresses PTI’s customer list.

- A memory-cycle turn that hits conventional packaging and removes the free-option leg of the thesis.

- ROE failing to step up despite the capex bet by 2027.

10 The one number: the FOPLP ramp, qualification in 2H26, volume from 1H27

The FOPLP ramp: customer qualification in 2H 2026, then monthly panel output against the ~6,000-panel build-out through 1H 2027. We are precise here because the tape has not been: first-phase panel equipment arrives this summer, qualification is a second-half event, and volume is a 2027 event, so a mid-2026 “ramp” headline in either direction is noise. This schedule is the cleanest proof point that the capex bet is converting into capacity and that the CoWoS overflow thesis has physical inventory behind it. If qualification lands in 2H 2026 and output scales on the 1H 2027 schedule, the bull case is intact and we would add on weakness. If it slips, the multiple starts to look foolish, and ASE will be shipping panels first. Either way, we wait for our accumulate line near NT$272 to NT$285 before we pay for the ramp.

Step back once before the desk section, because the shape of this trade is the shape of the whole build-out. On our worldview the binding constraint keeps migrating down the stack: transistors were the chokepoint until 2024, CoWoS packaging is the chokepoint now, and the next squeeze is already visible in panel formats, HBM test intensity and, from late 2027, hybrid bonding. Each migration re-prices a new layer, and each opens a window for whoever built capacity just before the constraint arrived. PTI is a bet on exactly one of those windows. Windows are real money, but they are rented, not owned: the durable rent lands with whoever holds the qualified interface when the constraint moves again, which is why the equipment and materials one layer further down (the moulding presses, the substrates, the glass cores) keep showing up as the better chokepoints in this series. Pay for a window only at a price that does not need the window to last. That is the whole discipline behind the NT$272 to NT$285 line.

11 If you want to trade it: expressions, not chases

The verdict above is the position: we own nothing here and bid at NT$272 to NT$285. For readers who run books rather than watchlists, our desk pass turns up four expressions worth testing, with the numbers computed deterministically from the tape (realised volatility, pair z-scores, betas), not eyeballed. Treat them as ideas to test, never recommendations, and size for a stock whose 30-day realised volatility is running near 91%, up from 75% over 90 days. There are no listed options on this line, so every expression is cash equity.

- The core expression is the limit order. Sell strength in the NT$333.5 to NT$362.5 zone if you own it, and bid the accumulate band at NT$272 to NT$285. Every reference level we compute, the DCF-weighted NT$296, the Street average NT$277, the EPS-weighted NT$272, sits below the price; a stop above the NT$362.5 Street high caps the failure case.

- The relative trade is long TSMC, short PTI. The pair trades off the same advanced-packaging driver, the spread sits mildly stretched (weekly z-score +0.77, pair beta 0.95), and the better-positioned owner of the constraint is on the long side. The honest risk: correlation is only 0.46, so the pair can decouple on a single PTI headline, and TSMC reports on 16 July, so the spread is best left alone until the peer reset clears.

- The statistical anomaly we are NOT taking. PTI versus ASE screens at a weekly z-score of −2.41, PTI cheap against its own history with its closest rival, which mechanically argues long-PTI short-ASE. We decline it, and the reason is the point: the fundamentals just moved against the statistics. ASE’s panel line targets volume two quarters ahead of PTI’s and it is already printing 20%-plus price rises, so some of that spread is a re-rating that deserves to stick, not noise that mean-reverts. When the quant signal and the second-source race disagree, the race wins.

- The patience play is a real position. PTI’s own second-quarter date is not yet confirmed, and its expected earnings-day move has historically been small (about 1.6% mean absolute over the last eight prints) against a 91-vol tape, so the event is not the edge. Cash, plus the alerts below, is the fourth expression.

For good order: none of this is investment advice, and the desk numbers above are the publisher’s own calculations from public price data.

12 Dates to watch

The July calendar is dense, and almost all of it is other people’s prints that read through to PTI. Dates are source-traced; PTI’s own results date was unconfirmed at publication.

- 10 July: PTI June monthly sales (Taiwan’s statutory monthly-revenue deadline). The sixth consecutive deceleration, or a re-acceleration, in the year-on-year rate is the first read on the second quarter.

- 16 July: TSMC second-quarter results. Sets the AI-capex tone and any CoWoS and CoPoS commentary moves the whole overflow complex.

- 27 July: Amkor second-quarter results. The US OSAT read-across, now carrying the ten-year TSMC Arizona agreement.

- 30 July: ASE second-quarter results. The single most important cross-read: the rival panel line’s ramp commentary and whether the 20%-plus quote rises are holding.

- Late July, unconfirmed: PTI second-quarter results, the margin print our number waits on.

- 23 September: Micron FQ1 results. The memory-cycle read for the conventional half of the business.

One layer further out, the schedule that decides the thesis: FOPLP customer qualification in 2H 2026, volume shipments from 1H 2027, ASE’s rival line at end-2026, and TSMC’s CoPoS now checking toward 2029 to 2030. The window is long enough to pay the patient and short enough to punish the late.

13 Go deeper

The public sources behind this note, if you want to take the thesis apart yourself. Each opens in a new tab.

The thesis: CoWoS overflow to Powertech.

- TrendForce: TSMC CoWoS crunch pushes US AI chipmakers to Powertech through 2027 · the core overflow-valve report.

- TrendForce: AMD Zen 7 with Powertech FOPLP reportedly under evaluation · the most recent customer signal.

- TrendForce: ASE targets FOPLP mass production by end-2026 · the rival line running two quarters ahead.

- TrendForce: ASE raises advanced-packaging quotes by more than 20% · overflow pricing power, printed.

- Taipei Times: chairman Tsai on the FOPLP schedule · qualification 2H26, shipments from 2027, from the company itself.

The technology and the competition.

- TrendForce: FOPLP heats up, ASE and Powertech expand, TSMC preps a 2026 CoPoS pilot · the case that this is a second source with no monopoly.

- TrendForce: FOPLP trial yields reportedly reach 90% at Powertech · the yield question that decides the ramp.

The capex bet and the roadmap.

- DigiTimes: Powertech lifts capex to US$1.6bn for AI packaging · the April 2026 guidance raise.

- DigiTimes: AMD and Broadcom back Powertech’s FOPLP; monthly revenue toward NT$3bn · the named backers.

- DigiTimes: Powertech secures full FOPLP bookings ahead of its expansion · the P11 6,000 panels/month target.

- DigiTimes: Powertech to accelerate FOPLP, mass production targeted 1H27 · the P12 roadmap.

The company, the cycle and the worldview.

- Yahoo Finance: Powertech (6239.TW) · live price, valuation and financials.

- Taipei Times: Micron’s acquisition of Powertech’s Xi’an plant · the 2023 Xi’an transfer.

- Situational Awareness (Leopold Aschenbrenner) · the structural AI-build-out worldview this note reasons from.

Not investment advice. For information and discussion only, and not a personal recommendation, offer or solicitation. Capital is at risk, and investments can fall as well as rise. The scenario fair values and price targets here are the publisher’s estimates, not a forecast or a guarantee. Do your own work.

All figures come from Powertech’s public disclosures, peer public market data, and the publisher’s own calculations. No third-party research is quoted or reproduced. Sources: Situational Awareness; Powertech public disclosures; chokepoints.ai scenario and DCF work. © 2026 chokepoints.ai · Issue 004 · Powertech sits at the advanced-packaging layer of the AI chokepoints map. All issues